| ||||||||||||

How much will it cost? It’s a sensible question from any consumer for any product. In the case of a life insurance policy, the answers are “it depends” and “probably less than you think.”

The “it depends” part relates to the type of life insurance involved and your personal circumstances. The “less than you think” element is based on industry research over the years that consistently shows most people overestimate the cost of insurance.

Overestimation: Guessing wrong

For example, in a 2025 survey by LIMRA, respondents were asked to estimate the cost of a $250,000 20-year term life insurance policy for a healthy 30-year-old male.

- Over half would estimate more than three times its actual cost.

- The average cost of such a policy is around $185 per year (less than $16 a month).

“The majority of Americans overestimate the cost of life insurance … It is clear, if a person hasn’t spent time shopping for a policy, they have no idea how much it will likely cost them in premium,” LIMRA commented when it released the findings. It has conducted its annual survey for more than a decade.1

Additionally, the research indicates that the younger you are, the more likely you are to overestimate the cost.

Cost factors: Type of insurance

Different types of life insurance involve different levels of cost.

- Term life insurance is the least expensive. That’s because it only provides basic insurance coverage for a set number of years – the “term.” The most common term policies are for 10 or 20 years, but terms of as little as five years and up to 30 years are also available.

- Whole life insurance tends to be at the other end of the price spectrum. That’s because it offers more in regard to protection and financial growth, assuming premium obligations are met.

Whole life insurance provides:

- Guaranteed lifetime protection. Lifetime protection can help protect loved ones or achieve legacy goals well beyond the specific, set periods prescribed by term insurance.

- Tax-deferred cash value accumulation. Cash value in a policy grows on a tax-deferred basis at a rate guaranteed by the carrier.

- The ability to borrow from cash value. This can provide a reserve source of funds for things like college tuition or supplemental retirement income.2

- The opportunity to receive dividends. Dividends can help build cash value, increase insurance protection, or help reduce out-of-pocket costs for a policy.3

Other types of permanent insurance typically range in cost between term and whole life insurance, although there can be exceptions. These include:

- Universal life insurance. This kind of life insurance offers a flexible premium, allowing you to adjust the amount you pay as long as you have enough account value. (Learn more)

- Variable universal life insurance. In addition to flexible premiums, this kind of life insurance has access to different investment options for your account value. (Learn more)

- Indexed universal life insurance. A kind of universal life insurance where credited interest can be correlated, with some caveats, to various market indexes. (Learn more)

- Group universal or group term life insurance. These are the kinds of life insurance typically offered by employers in benefit plans. They can fall short of individual needs and come with limitations. (See: Why group life insurance often falls short)

Individual cost factors

How much any type of insurance will cost you depends on your risk profile, which is primarily determined by your age and health. Generally, the younger you are and the better your health, the lower your cost. Gender is also a factor. Because women outlive men on average, life insurance for a female is typically lower.

So, how do these considerations play out in premiums? What's the difference between term and whole life insurance costs?

Let’s look at a hypothetical example of term insurance4 — typically the least expensive kind of life insurance. (Related: Buying life insurance on a budget)

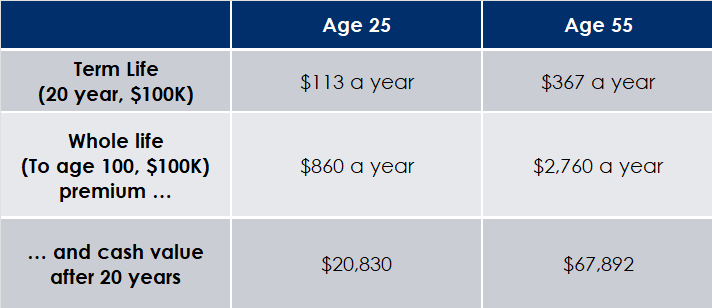

- The cost for a 25-year-old female nonsmoker in excellent health for a 20-year term policy for $100,000 would typically be about $113 per year.

- The cost for a 55-year-old female nonsmoker in excellent health for a 20-year term policy for $100,000 would typically be about $367 per year.

What about permanent life insurance that’s more expensive because it lasts a lifetime and offers more features?

Let’s look at hypothetical projected costs for a $100,000 whole life insurance policy where premiums are payable up to the insured reaching age 100.5

- The cost for a 25-year-old female nonsmoker in excellent health for such a whole life insurance policy would be about $860 per year.

- The costs for a 55-year-old female nonsmoker in excellent health for such a whole life insurance policy would be about $2,760 per year.

But remember, whole life insurance is permanent coverage and builds up cash value over time. The amount of cash value depends on the amount of the whole life policy you buy, how much has been paid in premiums at any given point, and the growth rate guaranteed by the carrier. Additionally, dividends can be used to increase both the amount of life insurance the policy provides and the cash value. Policies with fewer, larger premiums tend to build up cash value more quickly than policies with many smaller payments. (Related: What premium plan will work for you?)

In these whole life examples…

- The 25-year-old will have $20,830 in guaranteed cash value built up after 20 years.

- The 55-year-old, who would be paying more in premiums on a more constrained time frame, will amass almost three times that amount in 20 years.

To put it all together for comparison …

A MassMutual financial professional can provide you with a specific look at the costs for your situation.

Connect with a MassMutual financial professional

Other life insurance cost factors

Of course, other factors can come into play that would affect the cost of a life insurance policy, regardless of type.

For instance, life insurance needs typically evolve as you experience major life events like marriage, children, home purchases, or career changes. So the amount of coverage needed may rise. Changing the amount of the death benefit will change the amount needed in premiums. The more needed in benefits to help your family and loved ones, the higher the premiums.

And the addition of any riders — provisions added to a policy that provide specific benefits or features — can change the cost as well.

Also, occupation or lifestyle can be a factor. Smoking, which has been proven to adversely affect mortality, will increase life insurance costs. And high-risk jobs can be a challenge as well. For the Apollo 11 astronauts, for example, life insurance was too costly and they had to resort to other means to ensure that their families would get some support if their mission went awry.4

Conclusion

In the end, the cost of life insurance can vary widely, as a number of factors can come into play. More often than not, however, it is less than you may think. And given the protection and security it offers, plus the possible financial benefits available with some types, it can often be a meaningful asset in a family’s finances.

Frequently Asked Questions about life insurance costs

Q: What factors affect how much I'll pay for life insurance?

A: Your life insurance cost is primarily determined by age, health status, gender, tobacco use, coverage amount, and policy type. Additionally, your occupation, lifestyle activities (like skydiving), family health history, and any policy riders you add can influence your premium. Insurance companies use these factors to assess your risk profile and calculate appropriate rates.

Q: What's the cheapest type of life insurance?

A: Term life insurance is the least expensive type because it provides pure death benefit protection for a limited time without cash value accumulation. A 20-year term policy is often the most cost-effective choice for young families needing maximum coverage on a budget. However, "cheapest" doesn't always mean "best"—your optimal policy type depends on your specific financial goals and protection needs.

Q: How much life insurance can I afford?

A: A common guideline suggests life insurance should cost 1-3% of your annual income, though this varies based on your needs and budget. Many families find that even $50-100 monthly provides substantial coverage that ensures financial security for their loved ones. A MassMutual financial professional can help you balance adequate protection with affordability based on your specific situation.

Discover more from MassMutual…

Ultimate guide to life insurance

Buying life insurance to cover your parent

Single? 3 reasons why you still may need life insurance

___________________________

1 LIMRA, “2025 Insurance Barometer Study,” April, 2025. Quote based on MassMutual 20-year term policy.

2 Access to cash values through borrowing or partial surrenders will reduce the policy's cash value and death benefit, increase the chance the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured.

3 Dividends are not guaranteed. If the policy dividend option chosen is to reduce premiums, dividends will be used to reduce premium payments. If the dividend is not enough to pay the full premium due, the balance must be paid by the end of the grace period by the policyowner.

4 Quotes based on MassMutuall Term 20.

5 Quotes based on MassMutual Whole Life 100.

6 NPR, “What the Apollo Astronauts Did for Life Insurance,” Aug. 30, 2012,

.jpg)