| ||||||||||||

Prompted by marriage, the addition of a child, a new mortgage, or other life event, you’ve decided you need a life insurance policy. How big should it be?

The most straightforward way to help answer that question is to crunch numbers involving your dependents and your financial obligations.

This Life Insurance Calculator is a good starting point to help you figure out how much life insurance coverage you might need.

It will provide you with an overall estimate of your life insurance needs plus an analysis of how that overall cost breaks down to cover five critical areas:

But how well these estimates will actually meet your individual needs may depend on other factors. Here’s a closer look at each.

Income replacement

Life insurance can be used to replace a portion of your income if you should die prematurely. When purchasing coverage, however, many policyowners make the mistake of selecting a death benefit based on their current income without factoring in their future earnings potential.

That means they are only considering the life insurance coverage question in terms of what they need today and not what they will need to protect their family and loved ones in years to come.

“I always encourage my clients to think of the goals behind why they are purchasing the policy in the first place,” said Jeremy Thompson, a financial professional with Spectrum Financial Group in Dallas, Texas. “That usually drives the conversation about wages for the years they need to cover.”

Connect with a MassMutual financial professional

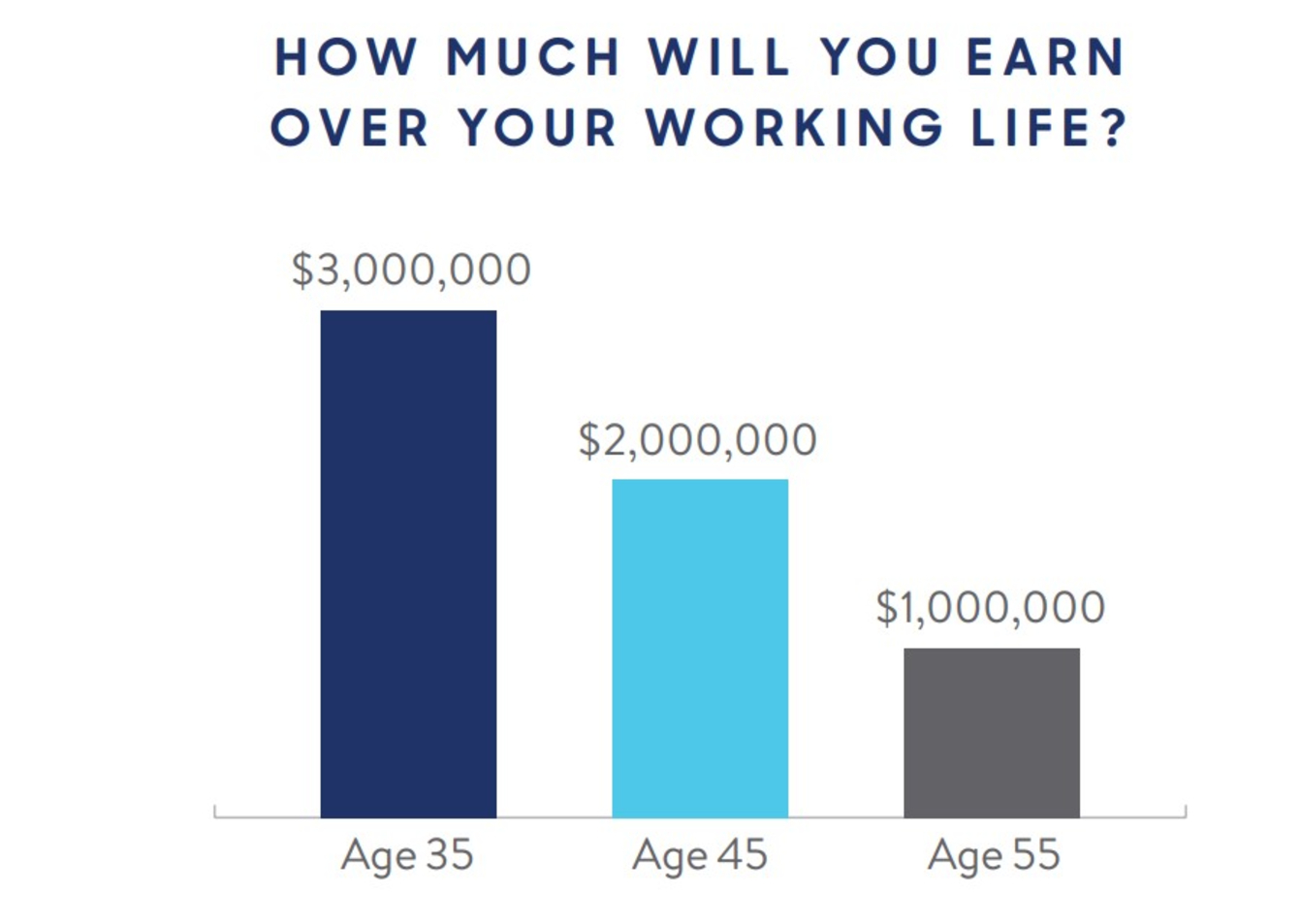

The following chart illustrates the aggregate income earned by someone starting at various age points and assuming they make $100,000 annually until age 65. It does not account for pay increases, inflation, taxes, the value of any other contributions, or the time value of money.

This chart shows the amount of future income over time. So, when thinking about how much life insurance you need, take into account that your coverage needs to protect the future income stream you would have provided to your family, and not just your immediate paycheck. (Related: What kind of life insurance should I get?)

Also, don’t overlook the need to fully insure a nonworking spouse or partner. Their contribution to the household translates into income. For example, the loss of a caregiving parent could translate into the need for a full-time nanny. (Related: Stay-at-home parents and the need for life insurance)

Income replacement tends to be the main consideration for many people in determining how much life insurance coverage to get. As such, it is usually the basis for various rules of thumb that typically propose a level of coverage based on a multiple (usually 10X – 15X) of your yearly income.

However, such blunt approaches can fail to take into account nuances of certain individual or family circumstances. A family with a special-needs situation, for example, may need much more. Also, the following considerations can have a major bearing on the question of appropriate coverage. (Related: Crafting a financial strategy for your special needs family)

Health and personal care for dependents

Beyond the loss of income, there are a range of costs that will need to be covered should you die prematurely. These items are often overlooked.

For example, there will be the loss of health insurance if your family is covered by your current employer’s plan. In the same vein, 401(k) and other savings programs will be disrupted. Replacing those health and retirement contributions could add up to more than $2,000 a month, according to the Insurance Information Institute.

And, if there are children involved, there will be a variety of immediate expenses, particularly childcare, that will need to be addressed. And beyond that are a range of expenses, like schooling or orthodontics, that may arise over the years. Indeed, the cost for a middle-class family with two children to raise a child born in 2015 to the age of 17 years will be $310,605, according to an estimate by The Brookings Institution.

Of course, the cost of possibly attending college can also add significantly to the costs that lie ahead for those children. Average published tuition, fees, and room and board for full-time, in-state students at public four-year colleges and universities stood at $11,260 for 2023-24, while the average private four-year college charged an average of $41,540, according to the College Board.1 (Related: A primer on college costs and aid)

Burial costs

The median cost of an adult funeral with viewing and burial was $8,300 in 2023, according to the most recent statistics compiled by the industry trade group the National Funeral Directors Association (NFDA). When the cost of a vault is added, something required by many cemeteries, the cost rises to $9,995. (Related: Funeral costs and considerations)

The NFDA’s cost estimates include the basic service fee, the removal of remains to a funeral home, embalming and other preparations of the body, a metal casket, use of the funeral home and the assistance from the staff during a viewing and funeral ceremony, use of a hearse for the body as well as a car or van for family, and minimal printed memorials, such as cards and a register book.

Of course, many other end-of-life expenses can come into play, depending on family circumstances and the desires of the deceased for final arrangements. And funeral costs can also vary regionally and be affected by competition. The Insurance Information Institute suggests planning for at least $15,000 in funeral costs and fees to wind up an estate.

The life insurance death benefit can be a big help to your family in covering those final expenses.

Mortgage

For many, especially first-time homebuyers, getting a mortgage usually involves co-borrowing — where spouses or partners both take responsibility for the loan. Sometimes, first-time buyers also need cosigners — typically relatives who will also agree to take responsibility to repay the mortgage.

In such situations, a premature death could saddle loved ones with an unmanageable debt load. And since mortgages are secured, mortgage payments must continue to prevent foreclosure on the home. It’s also important to stay current on property taxes and homeowner’s insurance.

As a result, people often ensure that their life insurance death benefit can help their beneficiary manage a mortgage obligation and other related expenses. Indeed, some couples starting out and buying their first home often look to term life insurance as a first step in establishing protection for one another. (Related: 4 times when term life insurance may be the answer)

Other debt

Variations in state law can affect what will happen to your debts after you die. In particular, if you live in a community property state, your spouse can be responsible for the debt that you took on during the marriage. Additionally, taxes and secured debt sometimes will a have to be paid outright.

Your debts become your estate’s responsibility when you die. If your estate doesn’t have enough money to repay all your debts, the relevant state law determines which creditors get priority.

Again, a life insurance death benefit can be a big help to your estate in paying off debts, perhaps fending off the need to liquidate assets like a family home or sentimental heirlooms.

Also, life insurance can make sure your heirs receive something when you die no matter how much debt you have. The death benefit your beneficiary receives from your life insurance, for example, is not considered part of your estate. It’s not subject to taxation, and creditors can’t claim it to cover your debts. (Related: 6 ways life insurance can help with estate planning)

Adding it all up

These five areas may not be the only considerations involved when deciding how large a life insurance policy death benefit should be. For example, someone may want to leave a significant legacy to their heirs beyond just supporting their basic living needs. Or, someone may have a favorite cause or charity they want to support.

But they do provide a rough idea of how much life insurance may be called for on a basic level. And the exercise might reveal that life insurance provided through an employer, while helpful, may fall short of actual individual needs, especially when family responsibilities are considered.

Beyond the size of the death benefit, there are other factors to consider when deciding on a life insurance policy. Various types of permanent life insurance can offer different features and involve different types of premium options.

Many people opt to talk with a financial professional about what might be suitable for their situation and how different types of policies can create a life insurance protection strategy that will provide the right amount of coverage over the course of their lifetime. (Need a financial professional? Find one here or let us know.)

Knowing the amount of coverage you’ll likely need is a good starting point for the conversation.

Discover more from MassMutual …

The power of a life insurance illustration

How whole life insurance helps diversify your taxes

_____________________

1 College Board, “Trends in College Pricing and Student Aid 2023.”

.jpg)