Today, we will have two main focal points. First, we’ll focus on the latest COVID-19 case growth and vaccine deployment (short version – it continues to improve), and second, we’ll explore the return and risk characteristics of cryptocurrencies.

With that, let us begin.

COVID-19: Where we stand

Every day, I follow the same routine. I wake up before anyone else in my family, make coffee, and begin to digest information from around the world. I tend to move between sources (Economist, NYTimes, Fox, BBC, Al Jazeera, and the like), and try to summarize the sentiment by country and by party. Inevitably, at this point, I feel depressed.

This leads to another cup of coffee and the processing of data. We retrieve data from around the globe and, after some quick data cleaning, I input that data into various models and begin to analyze differences between our predictions and reality. It is at this point that I, inevitably, begin to shake my head at the insanity between what I am seeing in the data versus what I am reading in the press.

The short version is that vaccinations continue to rise, cases and deaths continue to fall, while the press continues to paint a dire picture. While I can’t solve the latter, at least we can provide a bit of perspective on the former.

Enter charts 1 and 2.

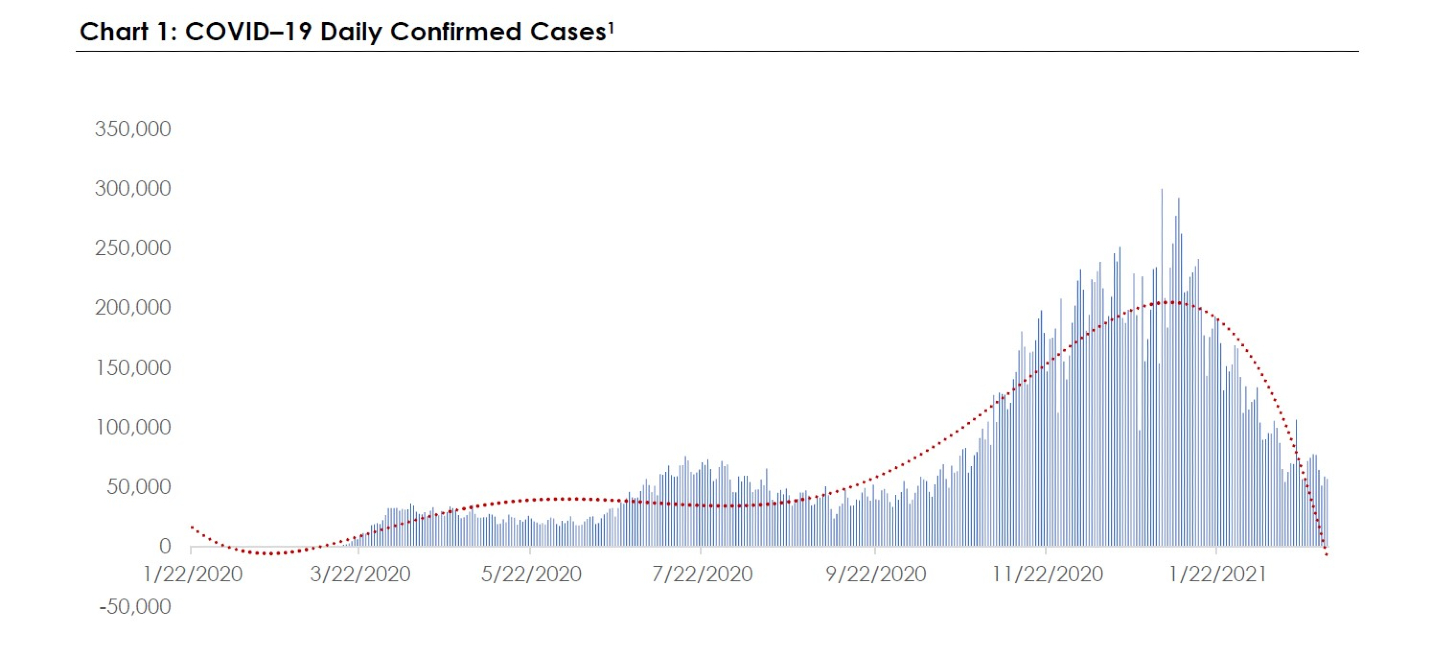

Chart 1 shows the total number of new confirmed COVID-19 cases per day in the United States. Within the construct that all of this is bad news, there is no way to argue this isn’t tremendously good news. One month ago, we were confirming more than 100,000 cases per day. Two months ago, we were confirming more than 300,000 cases per day. Yesterday, we confirmed a tad more than 50,000 cases per day. That is tremendous news. Daily case counts are falling.

To put this into perspective, the United States confirmed more than 6 million cases in December, and more than 6 million cases in January. In February, we confirmed a bit more than 2 million.

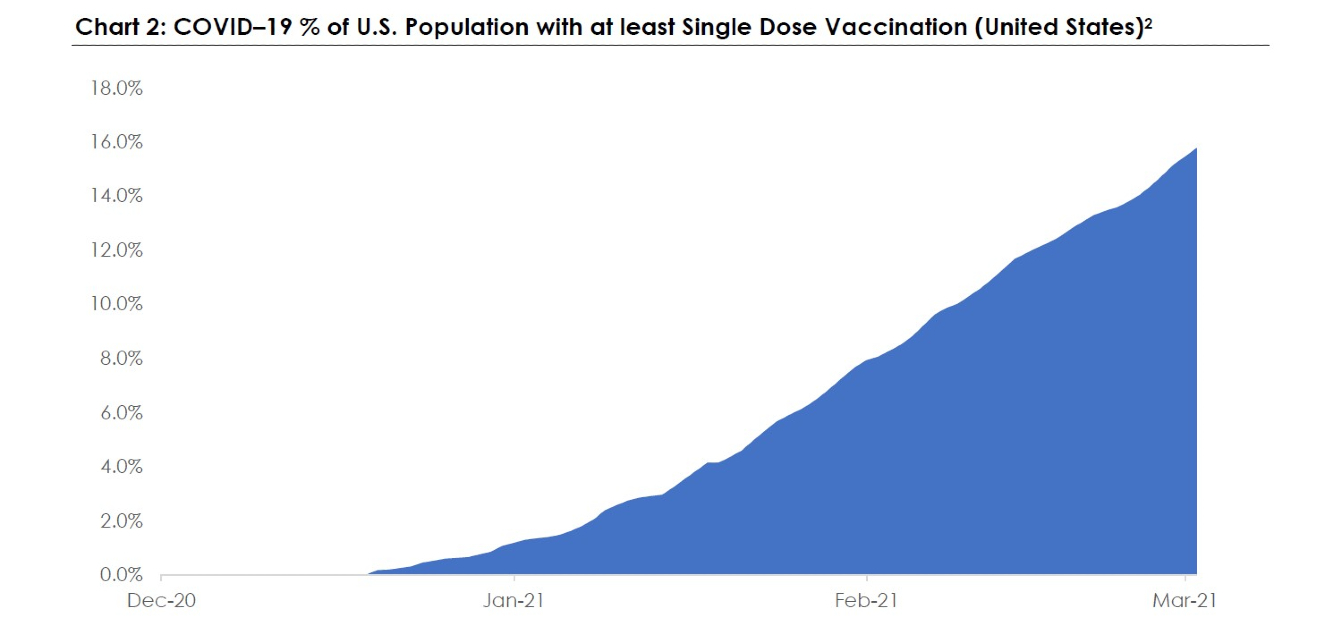

Chart 2 holds at least part of the explanation as to why.

Let’s put this into scale. On Dec. 1, there was not a single vaccine deployed. By Dec. 31, there were almost 300,000 vaccines being distributed each day. By mid-January, we had crossed the 800,000 vaccines-per-day threshold and, as of Thursday, March 4, the United States was distributing more than 2 million vaccines each day. In total, the United States has now vaccinated (with at least one dose) more than 50 million Americans. The scale is remarkable.

The chart above takes that data and converts it as a percentage of the overall United States population (men, women, and children). Again, remarkably, that means that more than 15 percent of the entire U.S. population has now received at least one vaccination dose.3

Further, as additional vaccinations are deployed, and as logistics continue to improve, this pace is likely to improve.

In short, optimism continues to build, and we continue to watch closely.

Bitcoin and cryptocurrencies

A couple of weeks ago, one of my sons came downstairs with a spring in his step. Normally a fairly reserved child, he bounded in and excitedly exclaimed, “Dad, we have to buy Bitcoin!” Given some of my recent work, I thought the timing auspicious and wanted to understand.

“Tell me more,” I said.

“Well,” he replied, “my friends and I were texting earlier, and a couple of them said they are getting rich because it just keeps going up. They said it, like, never goes down.”

I could think of no better allegory to start this analysis with.

Accordingly, what follows is an exploration of how Bitcoin has performed and how it has not performed.4 As with part one of this three-part series distributed a couple of weeks ago, I will try to remain objectively focused on the “what” and “why” and avoid the “what’s next.”

First, let’s explore what everyone seems to know, and then we will turn to what everyone should know.

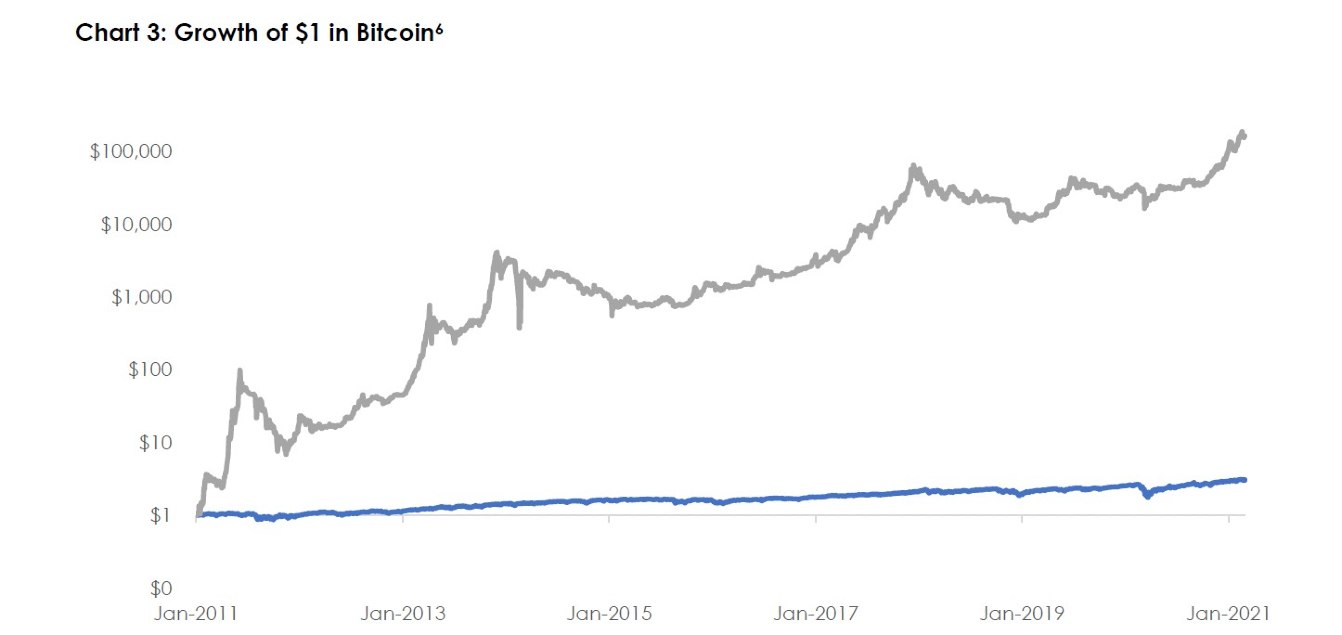

On the former, Bitcoin has provided a remarkable return to those that have been able to hold it. If an investor had started with $1 in 2011 and had purchased Bitcoin, that same dollar would be worth around $163,000 today.5 Over the same time period, if one had invested in the Standard & Poor’s (S&P) 500, that same dollar would have be worth around $3 today.

Chart 3 shows that depiction graphically.

This is, obviously, what piqued the interest of my son’s friends. This is also why, for example, several thousand new cryptocurrencies have appeared.

Before we rush out and buy our new Tesla (which, by the way, accepts Bitcoin now), let us breathe, and then take stock.

It has historically not been wise to purchase an asset just because it has gone up before we made the decision to purchase that asset. The fact that it has gone up is something we can only witness in history and does not, as we all know, guarantee that an asset will follow the same path in the future.

This dynamic is as old as trade itself, and history is replete with those examples. As an example, in 1636, in what is now known as the Tulip Bubble, tulips were being purchased at extraordinary prices simply because “others” were known to be “about to purchase” those same tulips. Perhaps unsurprisingly, tulip prices collapsed spectacularly when logic began to drive prices again, and buyers realized that tulips were really only valuable as flowers, not as financial instruments. While we can laugh at those crazy 17th century Dutchmen, let us remember the dot-com bubble of the late 1990s where companies such as Pets.com were being traded on ratios such as “price to mouse clicks” because, after all, there was no profit to be referenced.

Let me be clear. This is not to say that Bitcoin will collapse as the other examples have. This is only to say that to view the return of an instrument in history without considering the risk, or the likelihood of what that asset should do in the future, is a good way to lose large amounts of money quickly.

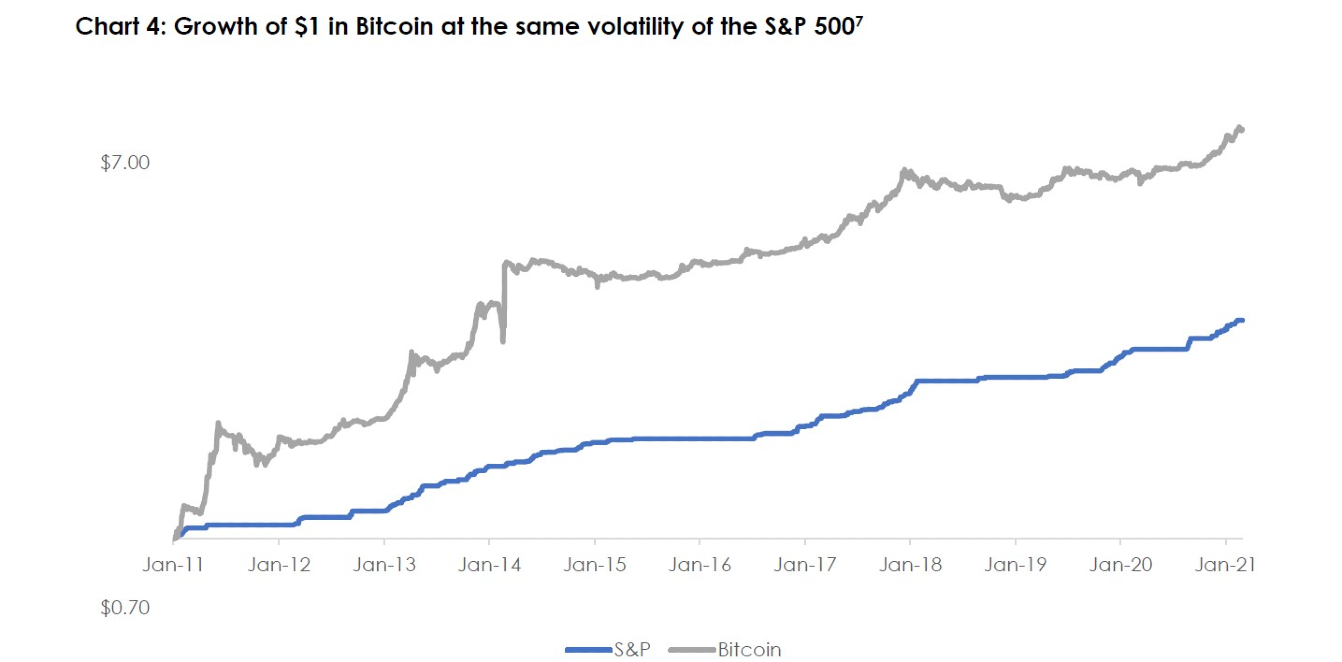

Therefore, let’s take these same two return profiles (Bitcoin and the S&P 500), and try to make them the same risk over the past 10 years. (For those interested in doing the same at home, I simply recalculate their returns to the same ex-post annualized standard deviation. This is the very definition of look-ahead bias but can be useful nonetheless.)

Chart 4 shows those return profiles graphically.

This chart tells a slightly different story. If an investor had started with $1 in 2011 and had invested in the S&P 500, the investor would be holding a bit more than $3 today (a good return). Yet had the investor been able to invest in Bitcoin with the same volatility as the S&P, that investor would now be holding a bit more than $8. Clearly that’s a better return than the S&P 500 (over this period) and has created significant amounts of wealth for those that have been able to hold it.

This then brings us to the last part of this analysis: the question of whether investors are emotionally likely to hold onto Bitcoin (and related cryptocurrencies).

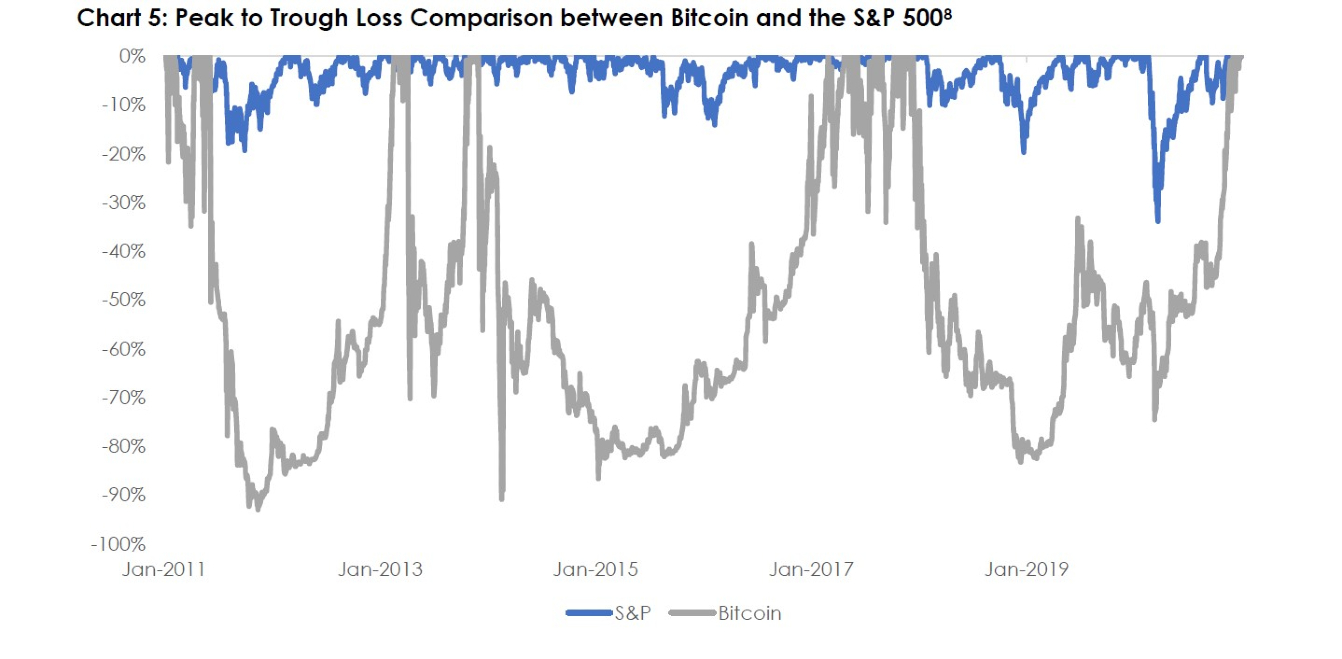

Ask any investor in the S&P 500 about their most painful experiences as investors and they are likely to talk about March 2020, or perhaps the crash of 2008, or maybe, if they have been investing long enough, Oct. 19, 1987. “Painful” they say.

Chart 5 helps orient that question a bit. The chart shows the peak to trough drawdown (or loss) by holding both the S&P 500 and Bitcoin. If an investor had $100 in the S&P 500 and lost 20 percent, the chart would show -20 percent on the axis. Once the asset recovers, the line moves back to zero, until it falls again. It is essentially a method to compare losses in different instruments.

Beginning with the S&P 500, the selloff of 2011 and the large and painful losses of 2020 stand out. As we all remember vividly, those were painful, quick, confusing, and hard to stomach (as evidenced by the number of investors that exited as losses mounted).

Turning to Bitcoin, there were nine distinct times over the past 11 years that Bitcoin lost more than half its value. There four distinct times that Bitcoin lost more than 80 percent of its value. If an investor held $100,000, after those selloffs, they now held less than $20,000. Those losses then turned into gains (eventually), but there was obviously no reason to believe they would have.

As a somewhat useless, but nonetheless instrumental, example, on Feb. 19, 2014, Bitcoin lost 57 percent in a single day. The day prior it had lost 30 percent, and the day before that it had lost 13 percent. Two days later, it made 129 percent back and, days later, on Feb. 24, Bitcoin again lost 47 percent. Confused yet? Not to worry…the very next day, Bitcoin jumped more than 330 percent!

Over the same time period, the S&P didn’t make or lose more than 2 percent in any single day, and cumulatively made roughly 1 percent.

Does this mean we shouldn’t use cryptocurrencies? No, not necessarily. It does mean it is vital we understand these are wildly volatile and should be treated as such.

To conclude, at the end of the last update, we ended with the following observations:

- Cryptocurrencies are remarkable innovations that have seen rapid adoption and significant increases in market value in a very short period.

- Bitcoin, and its brethren, are not assets that provide a risk premium. That doesn’t mean they aren’t useful, but they are simply mediums of exchange (also known as currencies), and not assets.

- As such, while cryptocurrencies go up or down sometimes, there is no structural reason to believe they will increase as equities, bonds, and real estate have done historically.

I would now like to add two more:

- Cryptocurrencies (Bitcoin in particular) have been remarkably strong performers over the past 10 years. There is no reason to believe they will, or will not, repeat that performance.

- Cryptocurrencies are wildly volatile. Since 2011, Bitcoin has been roughly nine times more volatile than the S&P 500 and roughly 30 times more volatile than bonds.9

In the next update, we’ll explore how (and if) to think about cryptocurrencies in a portfolio construct and how they can be accessed.

In closing, stay safe, stay focused on controlling what we can control, and save more than you think necessary.

Discover more from MassMutual …

Understanding the basics of investing

3 tips to avoid locking in losses

_________________________

1 Sources: Bloomberg, World Health Organization as of March 3, 2021, dotted line represents 7 day moving average

2 Sources: Bloomberg, World Health Organization as of Mar. 4, 2021

3 Source: U.S. Census Bureau

4 Note. I am using Bitcoin as the primary reference for cryptocurrencies because, as of this writing, it is the most dominant.

5 Source: Bloomberg, Coinbase as of March 4, 2021

6 Sources: Bloomberg, Coinbase, OurWorldinData.org of March 4, 2021; note the logarithmic scale

7 Sources: Bloomberg, cointelegraph.com as of March 4, 2021

8 Sources: Bloomberg, cointelegraph.com as of March 4, 2021

9 Sources: Bloomberg, cointelegraph.com as of March 4, 2021