Frayser, a community in north Memphis, Tennessee, lies at the edge of a peninsula formed by two small rivers that merge into the Mississippi. Put on the map in the nineteenth century by the presence of a railway and propped up by the freight industry, the neighborhood blossomed into an archetypal middle-class American suburb by the 1950s. But in the subsequent decades, the decline of American manufacturing hit Frayser hard. Industry cratered and workers fled, seeking jobs elsewhere.

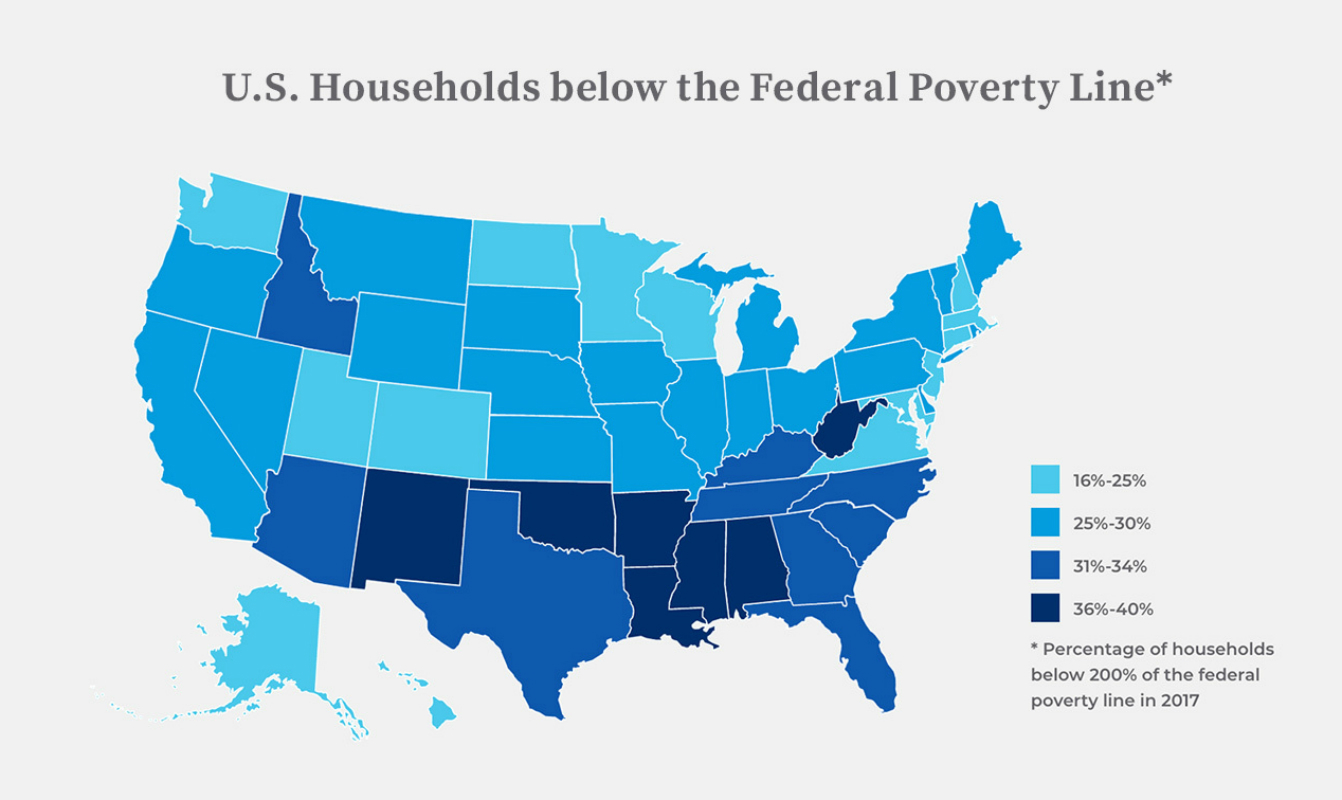

Today, Frayser’s per-capita income is lower than nearly 99 percent of U.S. neighborhoods. And, 85 percent of the children living in the community qualify for free or reduced-price school lunches.

Frayser isn’t wholly unique. Although the conventional wisdom is that the American economy is booming, many communities are being left behind. Known as financial deserts, these areas face entrenched structural barriers to development, including weak public transit and a dearth of affordable housing.

Those who call them home also struggle to gain access to traditional banking services. The reason is two-fold: Financial services firms are less available in distressed communities and, where access does exist, residents there lack sufficient income to build up savings.

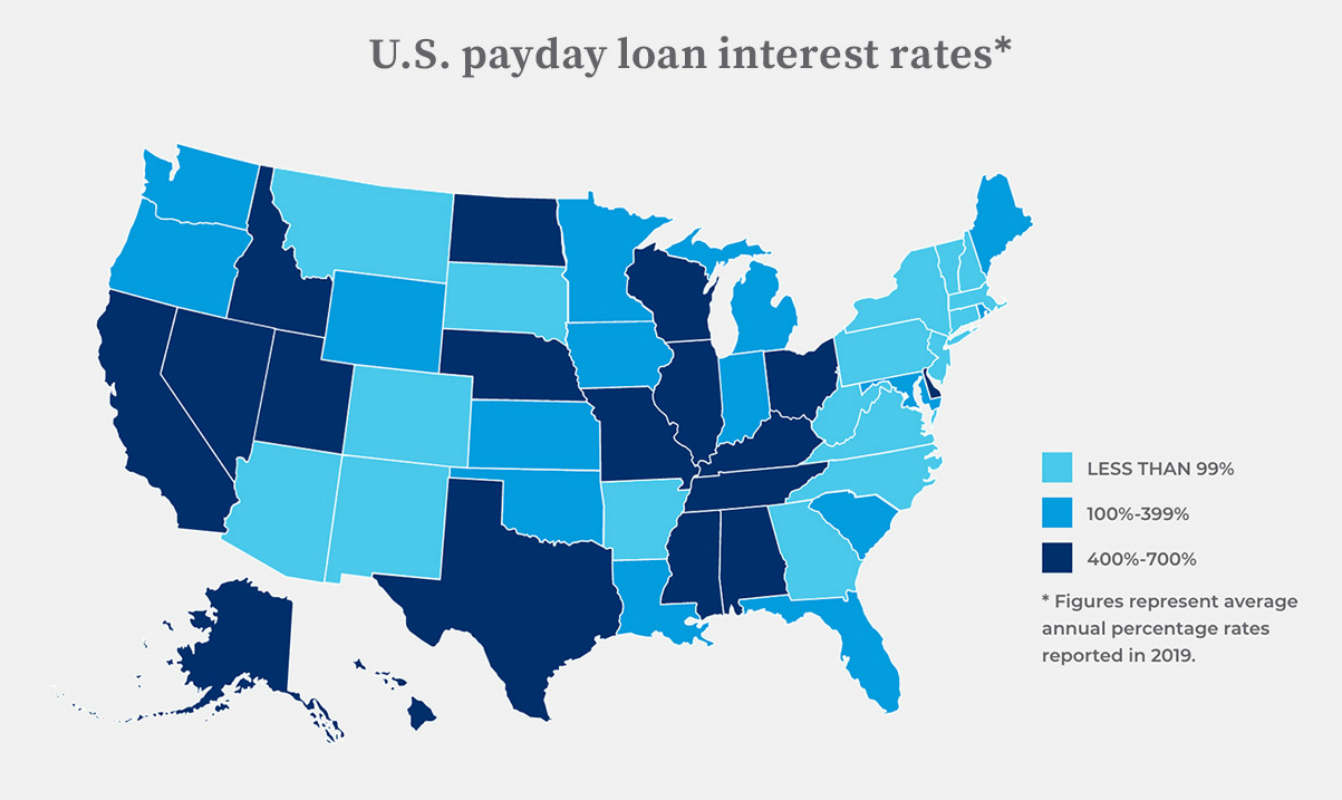

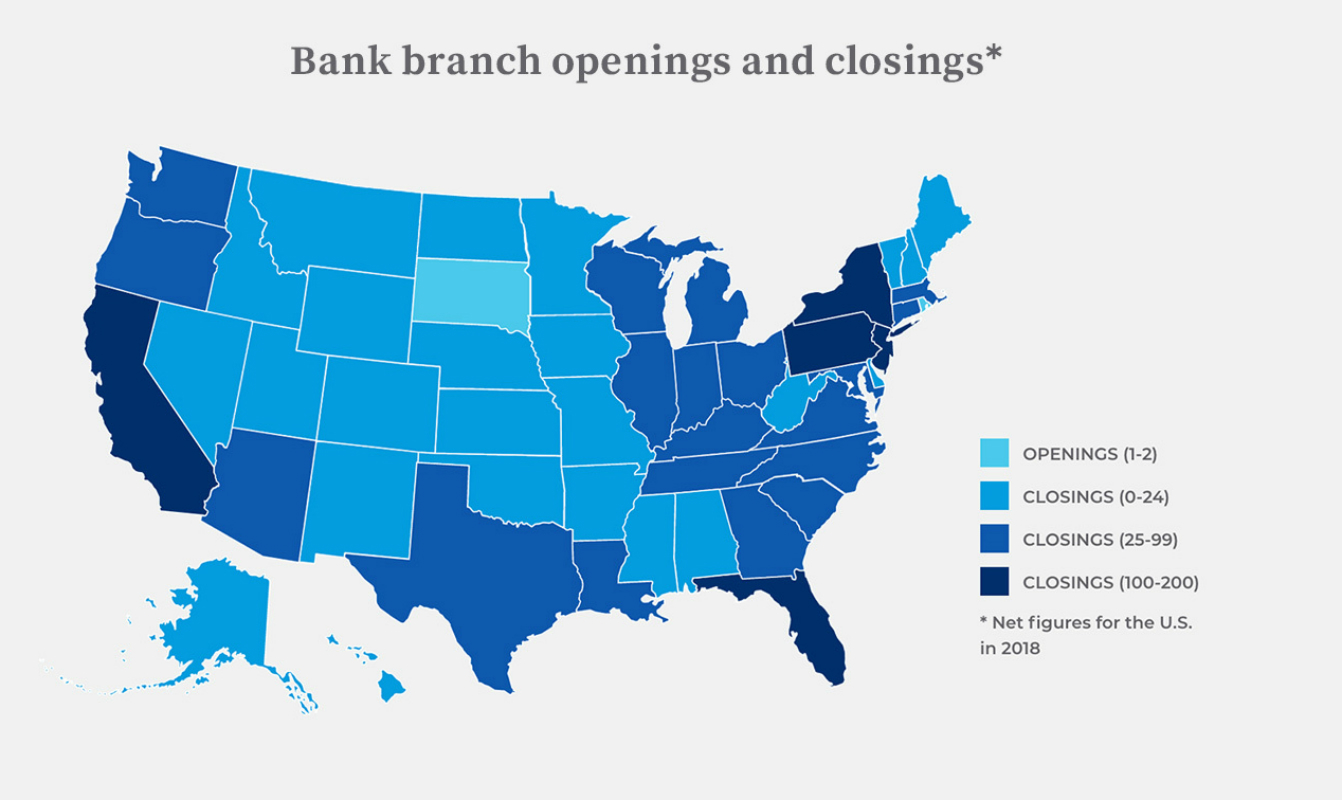

Absent a checking or savings account, and as banks across the country are closing their branches, Americans who live at or near the poverty line are forced to use alternative financial services when they need urgent cash or a loan, including pawn shops, title lenders and payday lenders, which typically charge annual interest rates of around 400 percent—and sometimes much higher. In Frayser, these offerings outnumber actual banks at a ratio of 8-1. Across the country, nearly one in four adults have borrowed money from alternative financial institutions. The result is a cycle of debilitating debt that hinders families’ capacity to build a better life.

However, innovative initiatives such as MassMutual’s Live Mutual Project are offering a sense of hope in financial deserts. Launched in December 2018, the Live Mutual Project is a comprehensive social impact program that connects community members to neighbors, resources and services in their neighborhoods to help navigate the oftentimes confusing and overwhelming environment meant to support residents. It is designed to help community members build a strong foundation for financial well-being today and for future generations by addressing the key issues that perpetuate cycles of poverty. The project is currently being piloted in two financially distraught neighborhoods, including Frayser.

“So many organizations have financial literacy training and other support programs in place in these communities, but when offered in isolation they’re not as effective as they could be,” said Jennifer Halloran, head of brand at MassMutual who leads the Live Mutual Project. “So, we asked ourselves: How do we support people who are on the brink of being able to get into better economic shape in these financial deserts? How can we, as a company, leverage our financial resources and expertise, and maximize our intended positive impact?”

Dispatches from the desert

Despite the relative growth of the U.S. economy as a whole over the past few years, many Americans are still struggling. According to one study, 78 percent of U.S. workers live paycheck to paycheck. For those in poorer communities, a stark absence of banks or credit unions only compounds their challenges. Owning property or starting a small business simply isn’t viable for the 16 million adults who don’t even have a bank account.

Many of these residents also don’t have access to conventional financial literacy resources. “I think we assume that people have basic financial literacy skills, such as the ability to create a budget,” said Annamaria Lusardi, the endowed chair of economics and accountancy at the George Washington University School of Business. “But we don’t teach this anywhere, so how do people figure it out?”

The lack of financial resources only exacerbates socioeconomic challenges in some of America’s most underserved communities. Take the North End neighborhood in Springfield, Massachusetts—the city that MassMutual has called home since its founding in 1851. The community, which hosts the organization’s second pilot program, has no bank and just a single ATM that runs out of cash daily. Jobs are hard to come by. At a time when the U.S. national average unemployment rate is just 3.8 percent, unemployment in some parts of the North End reaches 31 percent.

But statistics only offer a bird’s eye view of the situation. To understand what’s happening on the ground in this financial desert, one of the Live Mutual Project’s nonprofit partners, New North Citizens’ Council, brings together local representatives to discuss community challenges. These personal reports have given the Live Mutual Project team an invaluable perspective on the real conditions in the North End. One insight that came from these meetings was that funerals were a significant source of financial strife. Sometimes families are unable to raise enough money even to get a body released from the hospital. In response, the Live Mutual Project is bringing together the hospital, funeral home and New North Citizens’ Council to find solutions that will enable residents to deal with the financial challenge of losing loved ones without resorting to payday loans.

This in-the-trenches strategy developed from an organizational ethos that prizes working collaboratively with the community it aims to serve, said Dennis Duquette, president of the MassMutual Foundation. “We engage with the community, we listen, we build trust, and we act,” he noted. “Rather than come in and say, ‘Well, we’re MassMutual, and we know what the problem is. You need to do X, Y, and Z,’ we’re really taking more of a community-organizing approach.”

Designing community-specific solutions

Part of why the Live Mutual Project rolled out its initiatives in just two financial deserts is because its effectiveness depends on specificity. Duquette stresses that, because each community faces unique socioeconomic challenges, top-down solutions conceived in a boardroom and replicated across the country simply won’t work. You need an approach that’s informed by local perspectives and tailored to each area.

When the Live Mutual Project examined the financial landscape in Frayser, they realized they could start by helping the community in two mutually reinforcing ways. The first way was to offer funding to local organizations already doing important work, such as RISE, a nonprofit that offers a savings incentive program coupled with basic financial literacy coaching. The second way was to have MassMutual Foundation leverage its networks in Memphis to encourage local groups to work together to support their common cause.

“[Frayser] is a place where there are several strong organizations, but they don’t have clearly defined shared goals or capacity to take time away from daily programming to work on strategic partnerships,” explained Halloran. “When you make these connections and bring them together, you give them that forum for success. They just become stronger and more sustainable.” (Related: Fighting poverty through relationships)

While they’re still in early stages, Duquette said that the pilot programs underway in Frayser and the North End of Springfield have already yielded positive results. In short, the Live Mutual Project’s hands-on, customized tactics are working.

“The paradigm of good corporate citizens as check writers just doesn’t fly anymore,” Duquette said. “We believe a collaborative assault on poverty, blending the wisdom and resiliency of the community residents with the unique strengths of corporate, non-profit, and public sector partners can and will yield creative, sustainable solutions. It’s a somewhat provocative approach, but we’re very encouraged, hopeful and excited by what we’re seeing already.”